Written By: Brandon Wipf

Supporting ALLL environmental factors presents a challenge for all financial institutions. Yes, the 2012 Interagency Guidance on ALLL highlights nine specific factors banks should consider, but there is little instruction on how those factors should or could be substantiated. With that, many banks end up over-documenting in hopes that a shotgun approach will satisfy examiners, or even the board.

Of the nine recommended environmental factors, most can be benchmarked to specific internal or external drivers, which then transform the exercise from qualitative to quantitative. However, the challenges of gathering required data and then being able to present it in meaningful reports is a definite deterrent. With access to loan-level data that is also easily segmented by FAS 5 pools, institutions can build out various trend reports, highlighting such metrics as delinquency, classifieds, growth and concentrations. Trend reports at the FAS 5 pool level allow management to monitor each specific pool, whereas most other asset quality reports provide only a general overview of the entire loan portfolio. Essentially, this approach views each FAS 5 pool as its own portfolio and allows management to gauge trends at a more appropriate level.

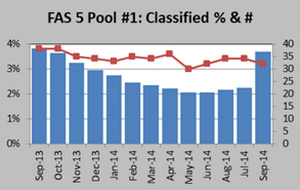

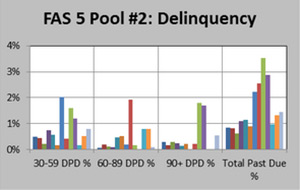

Banks can use this approach to support most of their environmental factors, as not all factors can be supported by quantitative measures. Quarter-end dashboards of rolling 12-month trends of the drivers for each FAS 5 pool could be prepared for management. This would allow them to compare the latest trends, along with the direction and severity of the historical loss rate to determine if a change to the environmental factors is needed. These drivers do vary slightly between consumer and non-consumer loan types, for reasons such as risk rating and loan approval processes. For example, with the “Problem Loan Trends” environmental factor, non-consumer FAS 5 pools have drivers such as Classified %, while consumer pools are more accurately measured by delinquency trends.

*Not actual performance data

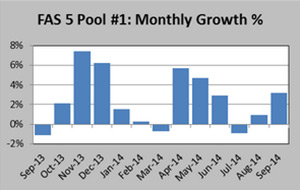

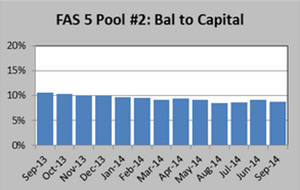

Continuing with this same logic, additional drivers for “Problem Loan Trends” include trends in Net vs Gross C/O % and Non-Accrual %, both displayed similar to the Classified chart above. A different environmental factor, “Changes in the Nature of Loan Profiles and Volumes”, is supported by a Monthly Growth % chart that concisely displays whether a pool experienced net growth, or maybe even a net contraction, for each of the prior 12 months. “Changes in Credit Concentrations” can be supported by the trend of FAS 5 pool balances as a % of Tier 1 Capital. Of course, the latter could be impacted by changes in the Tier 1 Capital figure, thus it may prove beneficial to have either a growth or balance dashboard for comparison.

*Not actual performance data

In addition to the performance and balance trends, banks can also track the number policy exceptions on approved loans to help support “Changes in Lending Policies and Procedures” as well as past due line reviews [on non-consumer loans] in support of “Changes in Experience and Ability of Lending Staff.” Both of these drivers can be presented in a similar dashboard style with monthly trends. The “Changes in Economic Conditions” factor can be substantiated by an economic analysis completed within the bank. This report may touch on unemployment, exports/imports, real estate activity, commodity prices and even gasoline prices, among other measures.

Environmental factor support is not simply in place to satisfy regulators, it can be a powerful tool to help bank management catch adverse trends before they grow into an issue. Since banks have determined that their FAS 5 pools are an accurate measure of homogeneous risk, it makes sense to allocate the resources needed to produce enhanced reporting on these segments. Additionally, as perceived loan concentrations emerge, more granular reporting may be required. For example, if a non-owner occupied CRE portfolio exceeds 100% of capital, it may be prudent to implement a property type or industry [NAICS] code to further diagnose the need for additional reserves via a related factor. Instead of viewing environmental factor support as an unnecessary burden, the process can be tailored to bolster a bank’s existing asset quality reporting function, with the added benefit of satisfying regulatory requirements.

About Brandon Wipf

About The Bank