A new Financial Accounting Standards Board (FASB) disclosure requirement makes several material changes to U.S. generally accepted accounting principles (GAAP). New requirements for determining the fair value disclosure of financial institutions’ loan portfolios are among the revisions.

(ASU) 2016-01, Financial Instruments – Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities, went into effect for financial statements beginning after Dec. 15. The guidance has already impacted public business entities at the beginning of this year. For all other institutions, it is effective for annual periods beginning in 2019 and interim periods beginning in 2020

The amendments require public business entities that have to disclose fair value of financial instruments measured at amortized cost on the balance sheet to measure that fair value using the exit price notion consistent with Topic 820, Fair Value Measurement. This change to GAAP eliminates the entry price method previously used by some institutions for disclosure purposes for some financial assets. Previously, GAAP permitted institutions an option to measure fair value in two different ways.

The FASB concluded that an entity is not required to revise its prior period disclosures of fair value for those financial instruments that may have been calculated using the entry price notion, which was an acceptable method under previous GAAP.

The new requirement also acknowledges that if an entity used an entry price notion to measure fair value in a prior period, then the disclosure of fair value in the periods after adoption of this new requirement may not be comparable with the new disclosures because those disclosures measure fair value using the exit price notion. In those cases, it was concluded that the entity should clarify in the notes to financial statements that the prior-period fair values disclosed are not determined in a manner consistent with the current-period fair values disclosed because of a change in the methodology.

The FASB sought to reduce the complexity and costs for public business institutions that are required to disclose information about fair values of instruments measured at amortized cost. An entity is required to disclose only the level of the fair value hierarchy within which the fair value information falls.

How vendors can help

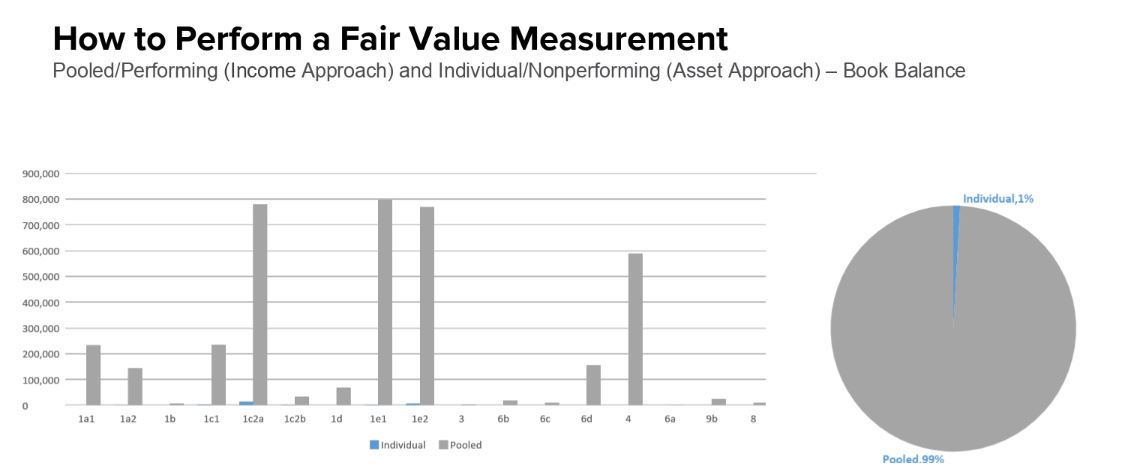

Neekis Hammond, CPA, at Abrigo described in a webinar last week not only what is required of the new standard but also how to perform a fair value option measurement. He touched on how various financial institutions handled the disclosures and valuation results in their Q1 2018 financial reports, and he provided an overview of current expected credit loss (CECL) synergies.

A demonstration of how to perform a fair value measurement from the webinar.

Reflecting on the benefits of using vendors, Abrigo CPA Hammond stated “Vendors can help to guide through this new requirement in multiple facets. Regarding CECL synergies, if a customer sends in one data file, it can be identified why that credit component is different explicitly and any questions that need to be answered can be addressed. A single software platform can accomplish both of those things. It is auditable and contains a controlled environment, yet still provides the ability to drill down to the loan level. Personally, as a reviewer, that is extremely important because doing cash flow modeling in a spreadsheet model is extremely painful. Lastly, vendors provide easily accessible visual aids if an institution receives questions from auditors.”

—

Neekis Hammond

Neekis Hammond as Managing Director with Abrigo, provides financial institutions with advisory services, leads thought leadership and consults with product development on compliance and accuracy. He specializes in the Allowance for Loan Lease Losses; CECL preparation and methodology; acquired loan accounting and valuation, Stress Testing, and various portfolio analysis topics. Prior to joining Abrigo, he held a key role within Elliott Davis Decosimo’s FIG Consulting division where he provided valuation, accounting and loan analysis services. Preceding Elliott Davis Decosimo, he was with a multi-billion dollar financial institution where he worked on acquisitions ranging in size from $130 million to $2 billion and was an auditor with a regional CPA firm.