10 Ways to get ready for CECL, as described by regulators

Jan 3, 2017

Federal financial institution regulators recently provided guidance on how they’ll view efforts by banks to comply with the FASB’s new current expected credit loss model (CECL). In a letter to financial institutions, the Federal Reserve, the Federal Deposit Insurance Corp., the National Credit Union Administration and the Office of the Comptroller of the Currency released a list of Frequently Asked Questions (FAQs) and answers related to CECL implementation.

Among the questions frequently asked, the regulators said, is how institutions can prepare for the implementation of CECL, which is considered the biggest change in the history of bank accounting. Here are 10 ways banks and credit unions can get ready, according to the regulators, along with available resources for learning more about CECL preparation:

- Get familiar with the new accounting standard. Educate directors and staff about CECL and how it differs from the current incurred-loss methodology. Abrigo has a complimentary CECL Prep Kit that aggregates industry resources and includes links, videos and other help for banks and credit unions as they familiarize staff with and prepare for the accounting change.

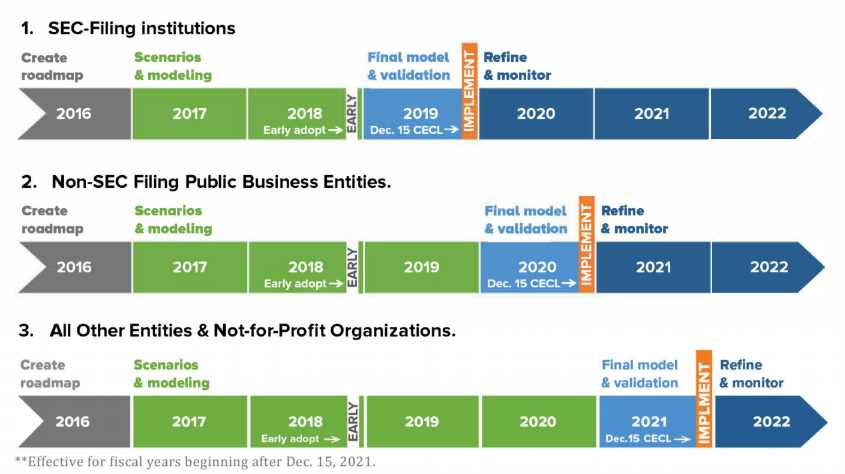

2. Determine the effective date that applies to your institution for CECL implementation. Below is a chart that shows when various institutions are required to begin using the standard for regulatory reporting:

3. Determine what steps are needed to implement the new accounting standard, and determine the timing required. Abrigo has provided examples of implementation timelines based on the various deadlines affecting financial institutions.

4. Identify the functional areas within the bank or credit union that should be involved in CECL implementation. Banking industry experts have said that developing accounting estimates used in the allowance for loan and lease losses will require increased involvement by credit risk management and staff, so developing cross-functional teams for CECL implementation may be useful.

5. Get advice. Regulators recommend discussing the new accounting standard with the board of directors, the institution’s audit committee and external auditors, with industry peers and with supervisory agencies. These parties can help determine the best way to implement the standard in a way that is appropriate for the bank or credit union’s size and for the “nature, scope, and risk of its lending and debt securities investment activities,” according to the agencies.

6. Look for leverage. Financial institutions ought to try to identify processes related to current allowance and credit risk management practices that can be leveraged as they apply the new accounting standard. “A move to the CECL model will require and reward increased collaboration between multiple departments,” Abrigo Senior Risk Management Consultant Neekis Hammond has noted. “The insights into prepayment behavior, life-of-loan loss, external correlations and possibly expected cash flows under some approaches represent an opportunity for banks to leverage valuable outputs for strategic purposes.”

7. The new accounting standard does not specify what method to use for estimating the allowance, so financial institutions will need to determine this, according to regulators. To learn more about the available CECL methodologies, listen to the replay of a recent Abrigo webinar, “CECL Methodology Series Kick-Off.” In the FAQs, regulators reiterated their expectation that “smaller and less complex institutions will not need to adopt complex modeling techniques to implement the new standard.”

8. Decide on data. Regulators recommend identifying data that should be maintained or added to collection efforts in order to implement CECL. “Examples of types of data that may be needed to implement CECL include: origination and maturity dates, origination par amount, initial and subsequent charge-off amounts and dates, and recovery amounts and dates by loan; and cumulative loss amounts for loans with similar risk characteristics,” the FAQs stated. Learn about other data elements that are recommended in the Abrigo guide, “Data for expected credit losses in the ALLL.” which is part of Abrigo’ CECL Prep Kit.

9. Identify any system changes that may be needed in order to implement the new accounting standard consistent with CECL’s requirements and with the methodology or methodologies that will be used to estimate the allowance.

10. Evaluate and plan for the impact on regulatory capital. Regulators said that upon initial adoption, the earlier recognition of credit losses under CECL will “likely increase allowance levels and lower the retained earnings component of equity, thereby lowering common equity tier 1 capital for regulatory capital purposes” at banks. The actual effect will vary by institution, however, and will depend on many factors, the regulators noted. Also, regulators noted that CECL implementation at credit unions will impact retained earnings at those institutions and will likely lower regulatory net worth. “However, it will not impact the measurement under the NCUA’s risk-based capital rule that becomes effective in 2019,” the FAQs said. “Under this new rule, the entire allowance balance will be reflected in capital for purposes of the new risk-based capital calculation.”

Regulators noted in the Dec. 19 letter that examiners may start asking institutions about the status of their implementation efforts. However, the agencies said examiners “will tailor their expectations based on the size and complexity of the institution” and the applicable effective date. “In doing so, examiners will be mindful of the scope and scale of changes necessary for each institution to make a good faith effort to achieve a sound and reasonable implementation of the new accounting standard,” the regulatory agencies said.