With the approach of the current expected credit loss model, or CECL, community financial institutions seem to have a grasp on the changes that they should be aware of come CECL implementation deadlines. Institutions will need to project credit losses over the life of the loan, and most are aware of the challenges they might face regarding available data, loss-rate methodologies and economic forecasting. Additionally, the standard is clear on the new way purchased credits and assets held for sale will need to be modeled.

Given that it’s been two years since the standard was released and given the abundance of CECL training resources that are now available, banks and credit unions might think they know all of what’s to come under CECL. However, these institutions should understand, and expect, the complexities that arise when the theory of the standard collides with the reality of community institution experience.

Garver Moore, managing director of Abrigo’ Advisory Services Group, recently conducted a CECL webinar that brought more than 300 executives with community banks and credit unions through exactly those CECL complexities that are not heavily publicized. He clarified these complexities through both accounting and regulatory perspectives.

Complexities tied to information selection

The standard states that “the measurement of expected credit losses is based on relevant information about past events, including historical experience, current conditions, and reasonable and supportable forecasts that affect the collectibility of the reported amount. An entity must use judgment in determining the relevant information and estimation methods that are appropriate in its circumstances”.

“There is a strong emphasis on the word estimate,” Moore noted. “Measuring credit losses based off available information is a big departure from what has been done in the past. FASB is very clear on the notion that institutions should thoughtfully come to a meaningful answer when measuring credit losses. There are really no handcuffs here on what information to use and how to use it; that’s up to us as practitioners.”

Complexities tied to adjustments

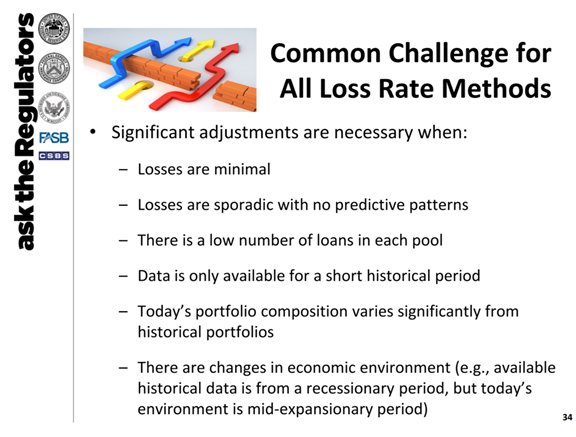

In February, there was an “Ask the regulators” webinar to discuss common CECL roadblocks. The regulators noted six scenarios where significant adjustments for credit losses will be needed, including when losses are minimal, losses are sporadic with no predictive patterns or there is a low number of loans in each pool. “These are the exact scenarios that apply more often — nearly universally, in fact — to community institutions,” explained Moore during the more recent Abrigo “Hidden Complexities” webinar.

That is another hidden complexity that can be avoided if thought through. As explained by Moore, the ability to produce meaningful quantitative results using loss-rate methods is proportional to both the size (count) of loans in the portfolio and the risk in the portfolio. For example, the application of loss-rate methods to large-dollar, underwritten portfolios secured by real estate will produce less meaningful and stable results than the application of that same method to high risk and/or high count portfolios.

Learn more about navigating the CECL transition.

Moore’s thesis is that “Given the effort required to implement any expedient methodology (loss rate, vintage, etc.), entities should not place themselves in a position to justify massive environmental/qualitative adjustments every quarter, forever. It is not much more work – and in many cases, significantly less – to implement a thoughtful, more sophisticated approach. This is design-time investment that returns in execution-time.”

For more information on not-so-obvious complexities related to CECL and how financial institutions can address them, listen to the replay of the webinar, “CECL: The Hidden Complexities to Simple Approaches for Community Institutions” or download the whitepaper, “Practical CECL Case Study: Hidden Complexities to Simple Approaches for Community Institutions.”

Additional Resources

Whitepaper: CECL Action Plans for Community Banks

On-demand Webinars: The CECL Methodology Webinar Series

About Abrigo