Data has always been the cornerstone of an accurate and compliant allowance for loan and lease losses (ALLL), and it will remain critical under the current expected credit loss model, or CECL. The Q1 2020 implementation deadline is approaching quickly for SEC registrants, and other banks and credit unions are making their own CECL preparations, but are financial institutions making enough progress in their CECL data collection efforts? How much data are financial institutions gathering for CECL, and will it be enough to support their calculations?

Data has always been the cornerstone of an accurate and compliant allowance for loan and lease losses (ALLL), and it will remain critical under the current expected credit loss model, or CECL. The Q1 2020 implementation deadline is approaching quickly for SEC registrants, and other banks and credit unions are making their own CECL preparations, but are financial institutions making enough progress in their CECL data collection efforts? How much data are financial institutions gathering for CECL, and will it be enough to support their calculations?

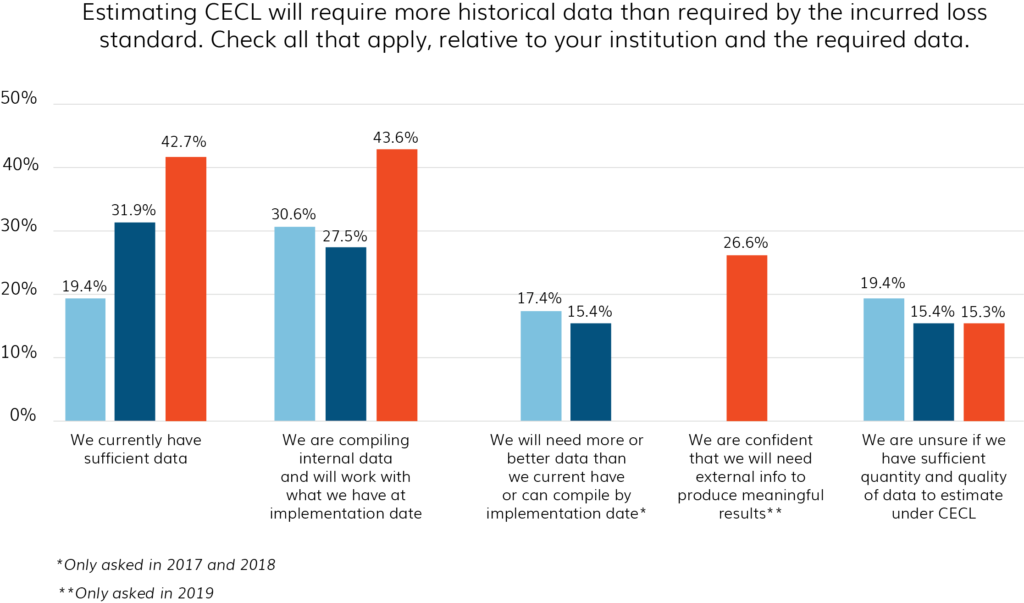

According to the 2019 Abrigo Lender Survey, nearly half of all financial institutions have collected and validated data as part of their CECL preparation efforts. However, only 43 percent of respondents expressed confidence that the data they have will be sufficient for CECL. Nearly 1 in every 6 institutions in the survey, including some SEC registrants, reported being unsure if they would have sufficient quantity and quality of data to estimate losses under the CECL standard.

“Whether a financial institution has enough or the right kind of data for estimating the allowance for credit losses under CECL will really be determined on an institution-specific basis,” said Paula King, Abrigo Senior Advisor and a former bank CFO and co-founder. “Our survey, however, found that many banks and credit unions have made good progress compared to institutions surveyed in previous years. By the same token, some still have work to do.”

While less than half of lenders were confident they have sufficient data this year, the share has improved from 2018 (32 percent) and 2017 (19 percent), so institutions are clearly making progress on gathering data for their estimations.

Unlike the incurred loss method for estimating the ALLL, the CECL standard includes a longer loss horizon, forward-looking requirements, and, depending on which methodology or methodologies a financial institution chooses for its portfolio, the need for access to loan-level data. For many institutions, this means capturing and archiving loan-level data to ensure they have the flexibility to try different methodologies in their tests and as they plan their potential capital adjustments.

King has noted that gathering the required historical data has posed challenges for many financial institutions. Core conversions, incomplete data fields, missing data fields, and a lack of historical losses in a loan segment or in an institution’s portfolio can cause problems with running a particular CECL model or being able to produce a meaningful result with a particular CECL methodology. In fact, some institutions have explored using the weighted average remaining life methodology, known as WARM or remaining life, in part, because it allows an institution to provide estimates for losses on segments with data limitations.

A larger share of respondents this year said they “are compiling internal data and will work with what we have at implementation date,” compared to previous years: 44 percent vs. 27 percent last year and 31 percent in 2017. There is greater recognition this year than in previous years that institutions may need more than what they’ve been able to gather internally in order to produce meaningful results. Twenty-seven percent of respondents overall (and 30 percent of SEC registrants) were confident they would need to incorporate external information to produce meaningful results. In 2017 and 2018 only 15-17 percent of respondents expected to need more or better data than they had then or expected to compile by implementation.

One of the challenges related to CECL and data collection is knowing what data is necessary and how much to collect. “Commonly in our field work, we see institutions chasing quantities and qualities of data that are not realistically achievable and may not even be necessary due to some generally preconceived notion regarding how much will be required,” Garver Moore, Managing Director of Abrigo’s Advisory Services group, said in the survey report, “CECL: Where Are We Now?” “The amount and the quality of information that you need depends on the story within that information, which is going to be institution-specific.”

“In an ideal world, we would all have our own internal, historical data with sufficient depth and breadth to support all our analytical and modeling needs,” said Regan Camp, Abrigo Senior Director of Advisory Services, in the survey report. “The reality, however, is that most institutions fall short of this ideal and thus, external data is needed to strengthen or augment the picture painted by internal data.”

HOW FAR BACK SHOULD CECL DATA GO?

Camp said that financial institutions are generally encouraged to gather and validate as much data history as is reasonably available, and they are particularly encouraged to look to secure data that spans periods of economic fluctuation. Many banks and credit unions have been curious about what that will mean in terms of the number of years of data collected by their peers.

According to the 2019 Abrigo Lender Survey, the largest percentage of respondents — 39 percent — plan to look back five to seven years to gather data. Only 12 percent said they would look back three years or less.

“Initially, for most institutions, the depth to which they’ll gather data will be less driven by subjective strategy and more by the objective reality of whatever history is available to them,” Camp said.

Two-thirds of survey participants representing banks with assets below $1 billion plan to look back seven years or less for their CECL estimation process. “Given the extended economic expansionary period, we find that most banks do not have enough loss or default experience in the last seven years to calculate a meaningful CECL result using their own bottom up data,” said Chris Emery, Abrigo’s Director of Strategy and Engagement. “This can certainly lead to challenges for these institutions, and may result in having to rely on primarily external rather than internal information to substantiate their CECL result.” Twenty-two percent of respondents from banks with less than $1 billion in assets expect to look back eight to 10 years to gather data.

Relative to smaller community banks, credit unions seem to be either more willing or more able to look back farther to gather data, with nearly a majority planning to gather eight or more years of data, Emery said. “This could be due to credit unions typically being more consumer-loan focused, as longer-term consumer loans may require more data to substantiate a meaningful CECL reserve estimate,” he said.

SEC registrants, too, plan to use data from a longer horizon. A majority plan to gather eight or more years of data, and only 37 percent plan to use seven years or less.

The FASB’s guidance for estimating expected credit losses is not prescriptive and, therefore, financial institutions will have latitude in how they calculate the reserve under CECL. However, loan-level data collection is a first step toward being compliant under future GAAP and toward having the flexibility to select the appropriate methodology for the institution and its portfolio. Institutions’ progress today on data collection will make a difference in their ability to implement CECL effectively by their respective deadlines.

For help on data collection methods, watch the webinar, “CECL Prep: Data Quality” or download the whitepaper, “CECL Prep Guide: Data.”

About the Author

Mary Ellen Biery is a Senior Writer and Content Specialist at Abrigo.